Property tax abatements: How do they work?

Property tax abatements are highly criticized, but the ins-and-outs of the process can be fairly complex. Learn how tax abatements work with a fictitious example in this explainer.

Jobs are the key to the economic and social health of a community. Employers make decisions to locate or expand their workforce using many criteria, including the property taxes they will need to pay. The 86 employers in the City of Columbus that received property tax abatements in 2020 created 3,713 new jobs in 2020, resulting in new annual payroll of $167 million.

Both the State of Ohio and the City of Columbus create policy initiatives hoping to attract permanent, well-paying jobs. Most of the responsibility falls on Ohio’s legislature and Columbus’ city council to pass laws that improve our economic development. Other programs are created by the governor or mayor within the bounds of their authority. School boards are also involved in approving which deals are accepted and how much employers will need to pay in lieu of taxes.

How development deals are made

Development administrators who work under the governor and mayor are continuously marketing the attractiveness of the area to potential employers using a wide variety of value propositions, including the availability of skilled workers, area educational quality, availability of improved sites, regulatory environment, and many others.

When an employer considers increasing their current workforce numbers in the area or moving to the area for the first time, they approach the development departments with details of their company’s planned project.

The administrators then evaluate the project to learn how many jobs the company expects to create and at what pay rate. After that, the administrators determine if the project is eligible for any existing job creation incentives in their toolbox and they ask their governing body for approval.

Tax abatements are attractive incentives for businesses

Administrators can use a variety of incentives to create jobs, including a provision to lower or eliminate various taxes the employer would have to pay for a negotiated time period. Collectively called abatements, these reductions can be applied to various taxes, including sales, income, property and excise taxes.

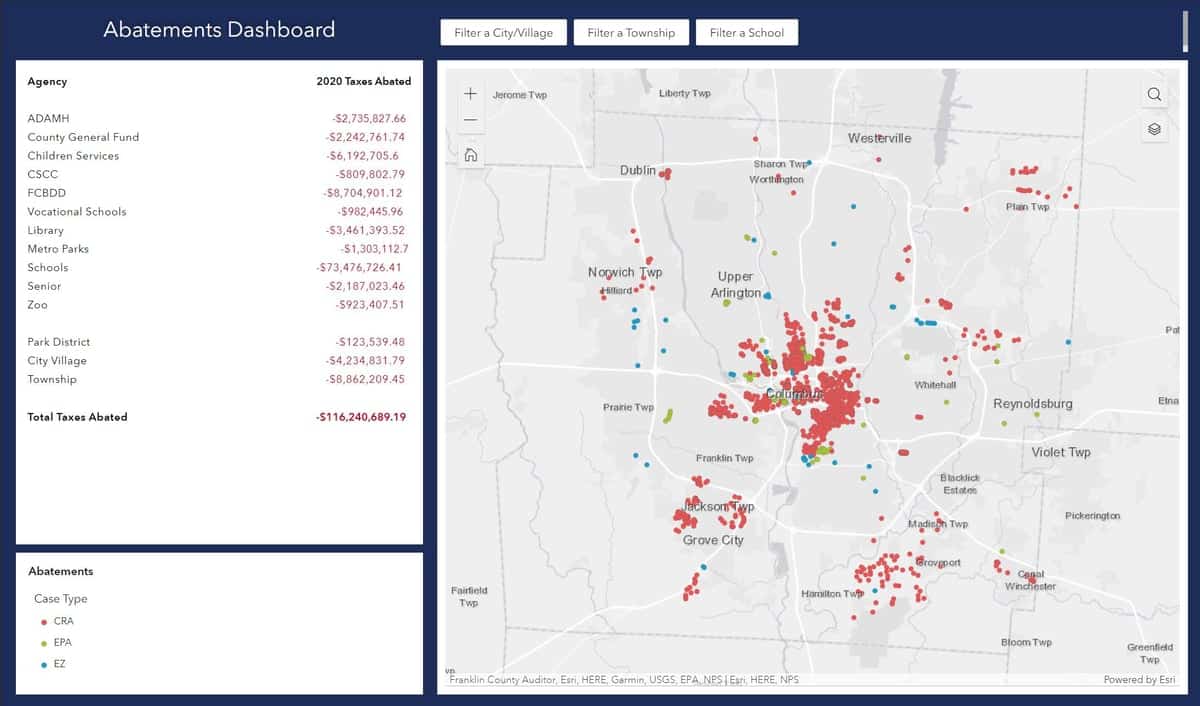

Click here to view the Franklin County Abatement Dashboard.

Most economic development does not qualify for tax abatements, according to Mark Barbash, director of the Ohio Economic Development Institute. For example, abatements are not usually available for retail developments or to create low-wage jobs, he said.

But for those employers who do qualify for an abatement, it is possible that they might have chosen to invest in the area without this incentive, which garners a lot of debate.

Who are employers accountable to?

The Franklin County Auditor keeps watch over the abated projects to make sure they are meeting their requirements in yearly meetings of the Tax Incentive Review Councils (TIRCs).

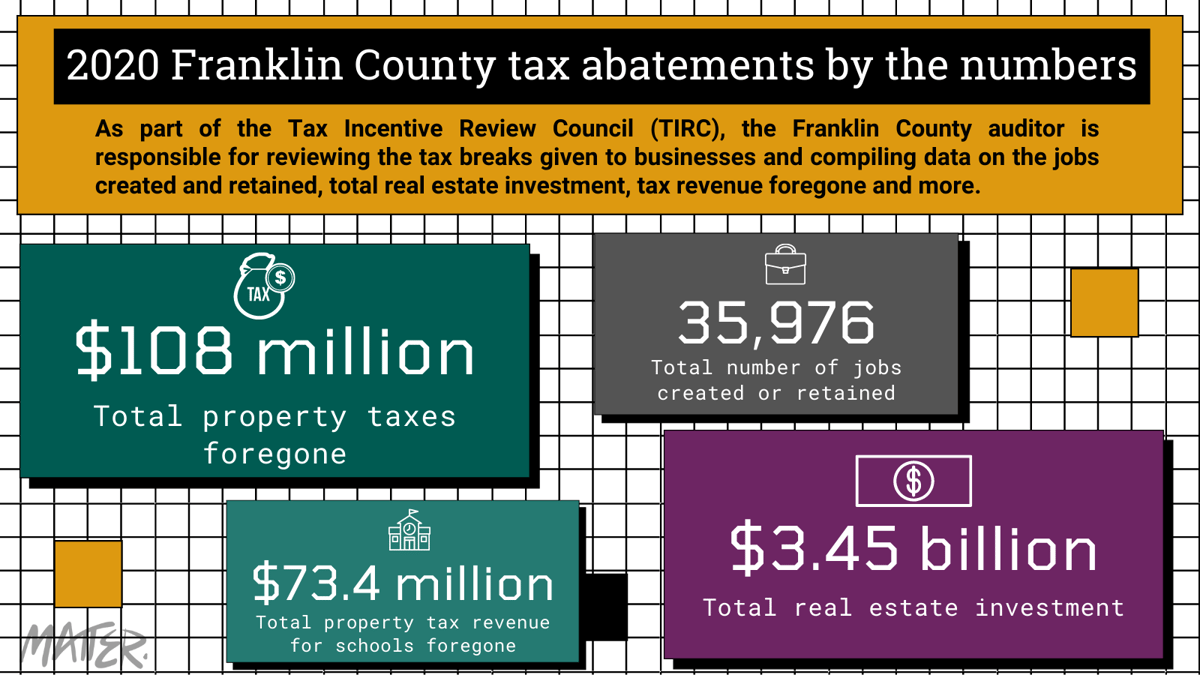

In 2020, the auditor’s office reviewed 532 abated or tax increment financing (TIF) county-wide projects that created or retained 35,976 jobs, representing nearly $1.9 billion of payroll that generated $47.5 million in direct income tax revenue.

Last year’s real estate and equipment investments totaled almost $3.5 billion. Investors received more than $108 million in tax savings, which is a little more than 5% of the total property tax collections in the county.

Ohio law requires school districts receive a cut of income taxes

For projects with over $1 million in yearly payroll, state law requires the city to pay half of the income tax collected from those new employees over to the school district where the employer is located, according to Michael Stevens, Columbus’ director of development.

In 2021, the City of Columbus will pay $2.3 million to various school districts based on 2020 receipts, he said.

For projects that abate over 75% of property taxes or go beyond 10 years, Stevens said the employer must negotiate with the school board for approval of the abatement. During that negotiation, both parties determine any additional Payment in Lieu of Taxes (PILOT) that the employer will pay directly to the school district on top of the share of income taxes that the city will send to the school district.

>> Our donors make everything you see possible. Want to support local, women-founded, independent nonprofit news? Donate here.

Breaking down how the cash flows in a development project

Tax abatements are not a simple process so here’s a quick look at how the money flows through this strategy.

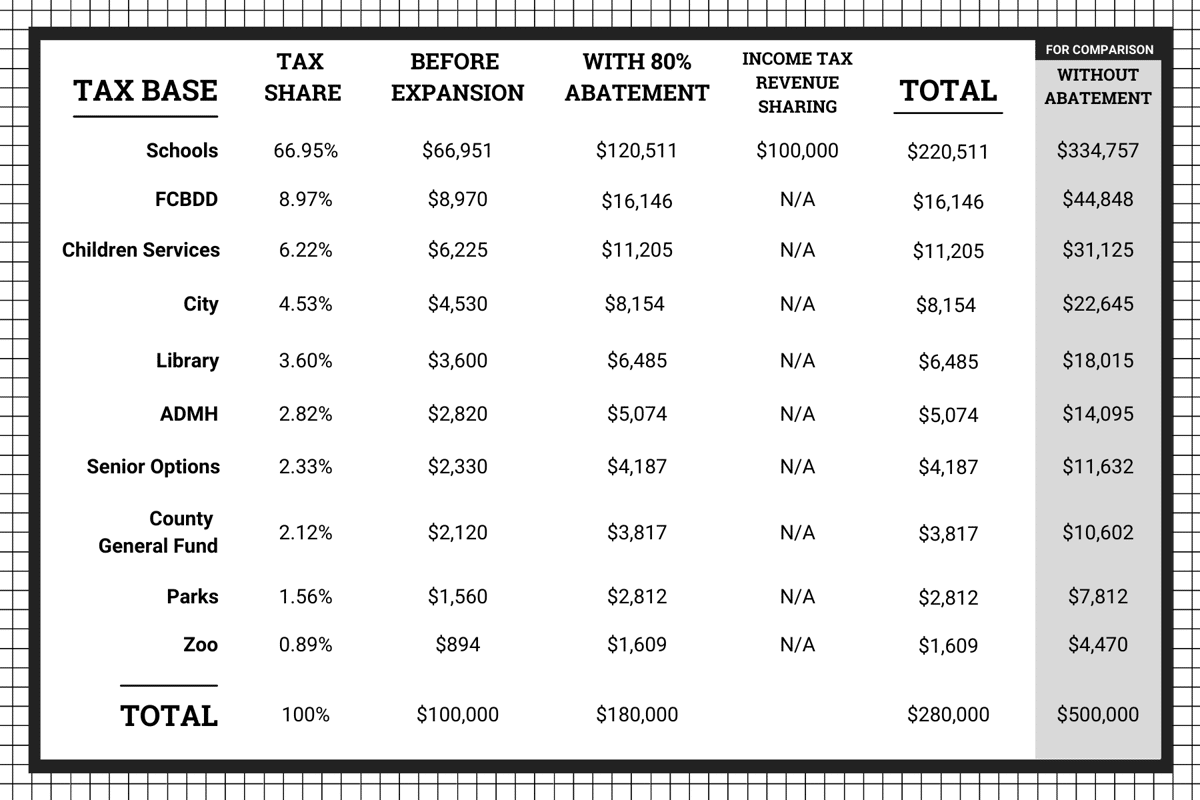

The chart below represents a fictitious warehouse that is expanding its capacity five-fold. Assume the improvement to the property will raise property taxes from $100,000 to $500,000. Also assume the employer’s payroll will increase from $2 million to $10 million.

Without a tax abatement, the total $500,000 in taxes on that property would begin to be paid to the county, and the school district would receive 66.95% of the $500,000 in property taxes or $334,750. (Note: The exact percentage — in this case, 66.95% — can vary between projects, so we’ve used this percentage to represent the Columbus City School district.)

With a tax abatement, the amount of property taxes abated would be a percentage of the amount above $100,000. For this example, let’s say 80% of the total $400,000 improvement project — which would be $320,000 — is abated for 15 years. Since the property tax abatement is above 75% and is longer than 10 years, the employer in this fictitious example would then be required to negotiate a PILOT with the school district it’s in — which, for this example, we’ll be using the Columbus City School district.

With this abatement in place, the employer would continue to pay the current $100,000 in property taxes, plus 20% of the abated $400,000 increase in property taxes, or $80,000. That’s a total of $180,000 in property taxes paid to the county — instead of the $500,000 in property taxes paid without an abatement.

The new employees would also pay 2.5% income tax on the $8 million of new payroll to the city, or $200,000.

With the abatement, the school district would receive money from four sources:

1) 66.95% of the $80,000 of property tax paid = $53,560

2) 66.95% of the original $100,000 of property tax paid = $66,951

3) 50% of the $200,000 of income tax collected from the new payroll = $100,000

4) 100% of the negotiated PILOT paid directly to them from the employer

With an abatement, the total money the school district would receive from the project would be $220,511, plus whatever money would be negotiated as part of the PILOT . Without an abatement, that total would be $334,750.

Do you have more questions about tax abatements? What can we answer for you? Send us an email at hello@matternews.org or submit your questions here.

Author

Related Articles

‘He was going to change the world’: Friends and family remember the life of Tomás Pacheco

The Columbus writer, who died on June 16 at age 24, leaves behind a legacy that those interviewed said will endure long after his passing.

In Ohio, who really gets a say in Anduril weapons factories?

Newly released emails show the strength of Anduril’s legislative influence in Ohio.

Local Politics: The small-time data center resistance

A petition to ban data centers statewide won’t be going to the ballot this year. So organizers are working locally instead.